Of course, this has wide-ranging ramifications for marketing and advertising – as well as a number of other sectors like travel, entertainment and FMCG.

To help marketers keep on top of what this means for them, their jobs and their industry, we’re collecting together the most valuable and impactful stats in this roundup, updated regularly since 20th March 2020.

Read on for statistics on retail sales, adspend, streaming subscriptions, social media use, recruitment figures and much, much more.

Alternatively, head over to our Covid-19 ecommerce stats roundup and our roundups focusing on fashion and grocery.

Contents

Latest

Amazon, Meta and Alphabet to account for half of ad market in 2025, thanks to acceleration from Covid-19

Thanks to a boost in social and ecommerce advertising over the course of the pandemic, new research from WARC Data suggests Amazon, Meta and Alphabet could account for half of a potential $1 trillion advertising market by 2025. 2021 saw what WARC calls a ‘meteoric rise’ in the value of the market, growing 23.8% year-on-year to total $771 billion. It is predicted to increase even further over the coming years, climbing 12.5% and 8.3% in 2022 and 2023 respectively.

In particular, heightened advertising in ecommerce settings is set to drive this trend. According to results from WARC’s survey of more than 1350 advertising professionals, two in every three marketers who already dedicate a proportion of their budgets to Amazon are expecting to increase their spend further in the coming four years. Heightened demand from advertisers has and is expected to steer cost per click upwards on the platform as a result.

Overall, most sectors were able to recover their pre-Covid advertising investments this year, while 2022 is expected to record higher ad spend than was reported in 2019, marking a full recovery for the industry. Travel and tourism is the most significant exception to this rule, having continued to struggle with restrictions, quarantine and testing regulations and hesitation from consumers throughout most of the year.

Travel ad spend set to grow at six times of overall ad market by 2023

One sector that has been continually affected by the ongoing Covid crisis is travel and tourism which, while seeing steady growth since restrictions were lifted earlier this year, has not yet seen a full recovery in ad investment versus pre-pandemic levels. However, Zenith’s latest Business Intelligence – Travel insights suggests there is reason for optimism as we enter 2022.

The sector’s nevertheless impressive double-digit growth throughout 2021 – 24% – is predicted to rocket even further in 2022 to 36% according to Zenith’s analysis. If this lofty expectation is reached, it could mean that the travel advertising sector could grow at six times the rate of the overall ad market between 2021 and 2023. Despite this, the travel industry will not meet or succeed pre-pandemic spending until the latter year.

It is expected that much of this increased advertising investment will remain dedicated to digital channels, with travel marketers having spent 63% of budgets on these formats in 2021 alone. This could rise to an even more substantial 70% by 2023, as more consumers grow accustomed to using travel apps and digital concierges. However, that’s not to say they are neglecting traditional mediums. In fact, 20% of budgets are spent on newspapers, magazines and OOH – well above the 13% budget ringfenced for these formats by the average brand.

UK advertisers set to spend record £7.9 billion this 2021 festive season

The Guardian reports new WARC figures that predict advertisers are set to spend £7.9 billion on marketing efforts in the three months to December, marking a new record since the study began in 1982. According to analysis, an extra £1 billion will be invested in advertising, equating to a 13% rise on last year’s advertising spend across the same period, which was somewhat subdued due to ongoing Covid-19 restrictions.

Spend on TV advertising is expected to increase by 9% to £1.56 billion, as brands battle it out with their headline Christmas ads. If this is indeed reached, it will signify the largest annual growth rate recorded by the vertical in more than a decade. Investment in search advertising could rise by as much as 15%, while online display may see a 12.7% increase. Together, these two verticals are set to account for 65% of all ad spend in the fourth quarter.

Overall, and perhaps unsurprisingly, cinema will experience the biggest bounce back in advertising spend, having been devastated by the impact of the pandemic and worsened by fresh lockdowns imposed in November and December. The category could see a huge 3160% uplift, as advertisers expect a boost from several much-anticipated titles and a high number of cinemagoers throughout the Christmas holidays. Meanwhile, despite OOH advertising suffering much the same fate as cinema over the last 18 months, advertisers are predicted to spend a respectable, if slightly muted, 50% more than they did in Q4 2020.

Advertising

Contact between clients and marketing agencies rose notably during the pandemic, but this has not improved relationship scores

Contact between clients and agencies inevitably rose during the height of the pandemic in H2 2020, but this has not been conducive to an improved relationship between the two, according to a report published by Aprais.

Data indicates that 35% of global clients contacted their agencies every day during this period, up from 21% in the first quarter of 2020. Likewise, the number of agencies that contacted clients every day throughout that six months rose to more than half (51%), compared to 31% prior.

Overall, agencies have said that working hours have been less respected as a result, with many clients asking for last-minute changes due to the uncertain nature of the global market. Meanwhile, the increased need for agency support among clients has led to a perceived lack of focus and an increased intensity of day-to-day tasks. High numbers of virtual meetings have also been cited by survey respondents, leading to a lack of time for ‘valuable discussion’ and a deterioration in mental health among marketers. Consequently, many agency staff have taken leave citing burnout.

By H2 2021, contact frequency between the two parties has reduced almost to pre-Covid levels, as old working patterns fully or partially resume, and more structured hours are reinforced.

44% of B2B marketers have ‘completely changed’ their marketing channel mix since the pandemic began

Data from Salesforce’s seventh annual State of Marketing report, this time covering trends in 2021, shows that 44% of B2B marketers have ‘completely changed’ their marketing channel mix since the pandemic began to meet new challenges and a shift in behaviour. Another 45% said that their mix had ‘somewhat changed’, leaving just 11% of B2B marketers’ strategies unaffected.

A huge 91% of marketing organisations now use social media as part of their mix, tying with digital ads as the most commonly used channel across the sector. Video is ranked third, with 90% of companies embracing the format, indicating that even more B2B marketers have been jumping on the trend in the past year in order to engage with their customers.

Notably, two-thirds of respondents also cited audio (e.g. podcasts and streaming ads) as a frequently used channel for their marketing efforts, emphasising the momentum this format has gained over the last 18 months.

When it comes to investment, 19% of B2B marketing budgets is now dedicated to advertising efforts, marking it as the category with the biggest share of spend. This is followed by tools and technology (16% share), content (16%), account-based marketing (16%), people (15%) and events and sponsorships (14%). By comparison, B2C companies spend a proportionally larger amount of their budgets on advertising (22%) and people (20%).

Overall, it appears that the survey respondents are optimistic about the direction their organisations are heading now that their strategies have shifted to more digitally-focused channels. Two-thirds of B2B marketers believe their companies will experience positive revenue growth over the next 12 to 18 months, while a further 30% predict growth to be stable. Just 4% expect it to decline.

Snap DAUs rise 23% year-on-year in Q3 2021, marking fourth consecutive quarter of >20% growth

Snap has once again seen rapid growth in revenue and Daily Active Users (DAUs) as we move into the latter half of this year. In a Q3 2021 financial statement, the social media company reported it was able to match the ‘record’ DAU growth rate it achieved in the quarter prior, and mark four consecutive quarters of >20% growth in the metric. This quarter’s 23% uplift equates to an extra 57 million users engaging with the app daily compared to the same period the year before.

Ad revenue remained high – up 57% year-on-year – but shows signs of slowing from the 66% and 116% increases it saw in Q1 and Q2 of 2021, respectively. This is thought to be largely down to Apple’s recently introduced ATT feature, which Snap CEO Evan Spiegel said had had a larger impact than first expected:

“While we anticipated some degree of business disruption, the new Apple-provided measurement solution did not scale as we had expected, making it more difficult for our advertising partners to measure and manage their ad campaigns for iOS.”

Further comments from Snap Executives shortly after the financial announcement included a note of concern surrounding the impact of global supply shortages on projected social media ad spend from brands. They said ongoing staffing, transportation and product shortages could prompt companies to hold back on spend across social platforms and opt to redirect budgets elsewhere during the crucial final quarter of the year.

Growth rate of Facebook MAUs and ad revenue continues to slow as life returns to ‘normal’

Facebook’s Q3 2021 financial statement shows the growth rate of Monthly Active Users (MAUs) on its namesake platform continues to slow, rising just 6% on the same period the year before to hit 2.9 billion. This marks the third consecutive quarter of decline for the metric, following a boost to engagement during the first wave of the pandemic in spring and summer 2020.

Family Monthly Active People (MAP) grew 12% year-on-year, matching the rate of growth reported a quarter earlier in Q2 2021, and indicating engagement remains stable across Facebook’s wider offering of social and messaging apps.

Despite a gradual decline in Facebook usership, total ad revenue rose by 33% over the three months to September, it remains several percentage points above pre-pandemic levels of growth. While, again, this third quarter figure represents a slowdown from the 50%+ figures revealed in Q2, this is in line with the company’s expectations that it would “decelerate significantly on a sequential basis as we lap periods of increasingly strong growth.”

It is yet unclear how much of this slowdown can be attributed to the consequences of Apple’s ATT versus a stabilisation of the ad market since global reopening began. However, the company has released a cautious outlook for its fourth quarter and full year financials “in light of continued headwinds” from ATT, as well as “macroeconomic and COVID-related factors”.

Q3 2021:

Online brands have increased TV ad spend by 37% since 2019

Brands that were born online have increased their linear TV ad spend by 37% since 2019, according to a report from Marketing Week which outlines new 2021 data from Nielsen and Thinkbox.

This trend varies in strength across different verticals. Online-born exercise brands, including the likes of Peloton and Echelon, have together increased spend on TV advertising by 279% in the two years, ranking this category as one of the most eager to use the platform. Meanwhile, spend by online car brands like Carwow and Cinch has collectively grown by 235% to reach £36.3 million in total.

Gifting and greetings cards, online food delivery services and streaming platforms also increased their investment in TV advertising by 209%, 194% and 137% respectively. Conspicuously, online travel brands cut their spend by 57% as they continue to feel the effects of travel restrictions.

Thinkbox’s Research and Planning Director, Matt Hill, commented that the overall increase in ad spend by online-born businesses has been mostly driven by the pandemic, but the rise in TV investment also “demonstrates they see [the format] as a valuable means of driving growth”.

While online brands are still making the most of the ecommerce boom, they are likely to remain using TV to boost their reach throughout 2021. By the end of the year, TV ad spend is expected to jump 18% on 2020, which declined by 11% versus pre-pandemic levels.

UK digital ad spend up 49% in H1 2021

UK digital ad spend rocketed to £10.5 billion in H1 2021, equating to a year-on-year rise of 49%, or a 42% increase on H1 2019, new analysis from IAB UK and PwC has revealed. This is the largest growth since IAB UK first began recording ad spend biannually, and spells positive news for the industry moving forward post-Covid.

It is thought that advertisers were better prepared for another national lockdown, which occurred in the early months of this year, enabling them to make more informed decisions about where to invest.

Search held onto its title as the biggest digital channel, with ad spend increasing 49% in this category compared to H1 2020, reaching £5.5 billion. Display performed even better in terms of growth – hitting 55%. Within this vertical, video display achieved almost 70% year-on-year growth alone, reflecting a growing consumer interest in video formats across the internet and on social media.

Mobile ad spend saw a 75% uplift as users continued to spend time scrolling and engaging with content. Consequently, smartphones now account for 64% of all digital investment, up from around a 55% share in the first half of 2020.

IAB UK’s CEO, John Maw, said of the findings, “We saw three years of change take place in just three months. Advertisers in turn adopted a more digital-heavy strategy as it was the medium least impacted by lockdowns. Meanwhile, the surge in video spend runs parallel to an explosion in short form video content and a move from advertisers to harness this as a vehicle for effective brand building.”

Marketing budgets now equate to just 6.4% of revenue

Gartner’s annual CMO Spend Survey, published in July 2021, has found global marketing budgets now equate to just 6.4% of overall company revenue, down from 11% in 2020. This marks the lowest ever recorded share as organisations continue to struggle with the effects of the coronavirus pandemic.

In a statement, Ewan McIntyre, Co-Chief of Research and VP Analyst in the Gartner for Marketers Practice commented, “Despite facing in-year budget cuts in 2020 due to the pandemic, most CMOs expected budgets to bounce back in 2021. This budgetary optimism was misplaced… However, these cuts have been a slow burn over the course of the last year, where many marketing budgets have not recovered what was originally lost.”

Until this year, marketing budgets have retained a relatively steady share of revenue, between 10.2-12.1% since the survey first began in 2014. Data from the study has shown that, regardless of company size and/or industry, no single organisation has escaped the need to drastically cut marketing budgets as a result of Covid-19. In fact, none of the brands that participated in the survey experienced a budget that broke into a double-digit share of total revenue.

Travel, hospitality, manufacturing and tech product companies, it has been revealed, experienced the largest budget cuts of all, while consumer products and goods came out the strongest, posting an average 8.3% share of revenue.

UK digital ad spend set to hit record growth by the end of 2021

The Q2 2021 Advertising Association/WARC Expenditure Report reveals UK digital advertising spend is set to hit a record 18.2% growth by the end of 2021, reaching a total £27.7 billion. This is an increase on prior April 2021 estimates that suggested a 15.2% rise and marks more than a two-percentage point lead on the current record of 15.9% reported in 1988.

If this new benchmark is met, it will recuperate the £1.8 billion decline in ad spend reported in 2020 and could pave the way for a healthy 7.7% additional rise in 2022.

Data also indicates that search will grow 19.7% and social media and display advertising by 17.2% over the same period. Naturally, the largest spurts will come from industries most affected by the pandemic – ad spend in the cinema category is predicted to skyrocket by 315.6%, while digital OOH could see a 43.7% increase.

In Q1 2021, ad spend rose just 0.8% year-on-year to £6.5 billion. This result is thought to be down to continued UK lockdown measures causing more large declines across some verticals and further increases across online formats. Despite this, predictions for the year end remain very strong, meaning (as we’ve already witnessed) the last six months of 2021 will be the biggest driver for ad spend growth. Of course, as spend accelerates this will have an impact on competition between brands, as well as ad pricing.

Travel industry doubles digital ad spend since January 2021

Travel Weekly reports findings from digital ad intelligence platform Pathmatics that show the travel industry has doubled its spend on digital ads since January 2021. Between 1st May and 20th August alone, total spending reached approximately $480.6 million, as travel brands advance their efforts to recover major losses from the past year.

In the full year to date (ending late August 2021), this figure rises to a total $844.7 million investment in digital advertising across the sector.

Expedia was the brand that spent the most over this period, splurging almost $94 million, followed by Disney Theme Parks and Resorts, spending $21.6 million. Meanwhile, popular accommodation and rentals app Airbnb came in at number three with an ad spend of $17.7 million.

According to additional data, Facebook was the top platform through which travel advertisers targeted potential customers between early May and late August, raising $157.5 million in ad spend. Instagram and YouTube were also very popular, drawing in $95 million apiece.

2021 UK ad spend predicted to be up 30% YoY

Following recent H1 2021 ad spend figures published by IAB UK, GroupM has revised its forecast for the full year. The media agency reveals it now expects ad industry growth to rise 30% year-on-year, 6% higher than what it predicted in its interim June forecast.

It said the amended figure was driven by even better than expected growth in TV and digital ad spend, meaning 2021 could record the third strongest year-on-year growth rate since 1955.

Drilling down by vertical, TV ad spend is now expected to rise 19% year-on-year, versus the 13% estimate made by GroupM back in June. Part of the reason for the uplift is attributed to summer growth spurred on by the Euros, as well as continued consumer interest in VOD sports content. Combined with this was a 28% increase in spend on TV advertising during the month of September, as almost all subcategories upped their investments.

Meanwhile, digital advertising could grow by as much as 34%, up by 7 percentage points on this summer’s previous estimate, due to digital platforms reporting high revenue across consecutive quarters. Furthermore, audio is expected to increase by 18% on the year before, as it solidifies itself as the next trend in online and social media content. Ad spend on print formats is still expected to decline, and while OOH has seen a substantial rebound in recent months, GroupM analysis suggests it will not be enough to return to pre-pandemic levels until 2022.

Other external factors like Brexit, staff shortages in the supply chain and growing Covid infections could also have an impact on the final numbers come the end of the year, although the report determined these factors to be ‘manageable’.

Q2 2021:

UK OOH advertising ad revenues soar 277% year-on-year in Q2 2021

The UK OOH industry experienced a considerable bounce back during Q2 2021, with revenues soaring 277% year-on-year, according to research from Outsmart and PwC. The figure is the biggest growth ever recorded for the vertical, reaching £198 million, following a challenging first quarter under lockdown which garnered revenues of less than £100 million by comparison.

Both traditional and digital OOH formats saw strong performance between April and June, with revenue growth of 339% and 247% respectively. As a result, digital share of OOH revenues has increased from 59% in 2020 to 63% so far this year – a ten percentage point increase on the pre-pandemic (2019) share of 53%.

As has been the case since the latter half of 2015, roadside locations accumulated the largest amount of revenue across all digital OOH environments in the second quarter, at above £80 million. Next comes retail and leisure venues at a little over £30 million, followed by transport environments at just £10 million (approx.).

Only roadside advertising, out of all three digital categories, has so far seen revenue significant enough (in the last 18 months) to match or beat levels recorded throughout 2019.

YouTube records growing year-on-year watch time via TV devices

As YouTube engagement remains high thanks to an acceleration in new viewing habits over the course of the pandemic, there has also been a substantial shift in watch time by device. This is according to a report from Conviva on the state of streaming in Q2 2021.

While mobile devices still account for the majority of unique views on the streaming platform – 63% to be precise – they only make up around half of total watch time. Instead, this quarter has seen a new trend in viewership via connected/smart TV devices, which account for almost a quarter (23%) of hours watched, despite only accumulating a 14% share of all video views. A similar trend can be found among desktop and console devices, although to a lesser extent: both have maintained a larger share of watch time than they have unique views.

As a result, watch time per view across connected TV and console devices is 1.96x greater than on mobile and tablet, while on desktop it is 1.46x greater. This points towards consumers increasingly choosing devices with larger screens to stream long-form content – something which, Conviva says, brands and marketers should make note of.

Many of these emerging viewing patterns have been formed over the past year, data reveals. In total, streaming growth reached 13% year-on-year as of Q2 2021, although this growth is disparate across device type. Share of hours watched via smart TVs jumped by 46% over the period, and connected TVs by 5%. Among devices with smaller screens, mobile saw a 30% increase, desktop 15% and tablet 9%. Interestingly, games consoles were the only type of device that reported a decrease in share of time viewed (-14%).

Social CPM grows 41% year-on-year in Q2 2021

Data from Skai reveals global social CPM has grown 41% year-on-year in Q2 2021 to an average of $6.37, after an equally large uptick in social advertising spend from brands. This is one of the highest costs per thousand impressions recorded in the last year, second only to 2020’s Q4 which reached $6.77.

Total social ad spend rose 41% on the same quarter a year before – the most badly-affected period throughout the pandemic – but increased just 3% on a quarter-on-quarter basis. Meanwhile, ad spend on campaigns designed to grow brand awareness, traffic and reach shot up 114%, driven by a 62% increase in CPM, demonstrating a shift away from campaigns that target direct action from consumers. Skai posits this new trend could have been largely caused by the introduction of iOS 14.5, which has made it much more difficult for marketers to successfully serve iOS users with targeted ads.

Despite the added cost for marketers, the overall number of social impressions remained flat year-on-year, although impressions for brand awareness, traffic and reach campaigns grew by almost one-third due to increased marketing efforts in this area.

This and other datasets on social advertising trends have informed WARC’s latest forecasts. It predicts total social advertising spend will grow by 10% as of the end of 2021, rising further to 12% in 2022.

2018 research shows how an advertising hiatus can impact brands’ long-term sales

Marketing Week reports recently released findings from a 2018 Ehrenberg-Bass Institute of Marketing Science study which demonstrates how an advertising hiatus can impact a brand’s long-term sales. Ehrenberg-Bass said in a statement that, likely due to the pandemic’s impact on brand advertising, it had had ‘subsequent interest from industry’ surrounding the results.

Using data from 70 Australian brands’ advertising spend over two decades, the study found that, on average, sales fell by 16% after one year without advertising. This rises to a 25% decline after two years and a 36% fall after three, before gradually levelling out over the remainder of the timeline.

The Institute admitted there were significant variables around the averages recorded, as only some brands saw an immediate decline in sales, while others saw a more gradual drop. Medium and large sized brands that were growing before deciding on an advertising hiatus continued to experience sales growth for 1-2 years after spending was cut. Small businesses, on the other hand, saw a more immediate detriment of sales, indicating an unsurprising ‘size advantage’ for bigger brands.

When the survey was conducted, there were just 57 cases where brands halted their media spending, 14 of which did so for a one year period. Of these fourteen, three saw continued sales growth during this time, while six saw a decline.

“Crucially,” Marketing Week reporter Michaela Jefferson says, “The study found that resuming advertising the next year did not stop this trend… suggesting it takes longer than 12 months to recover from a year’s hiatus.”

Although this research was carried out a while before the pandemic struck, it is essential to observe these findings given that many brands opted to pull their advertising efforts during 2020. After the events of the past year it will be interesting to see if the effects of such a mass advertising hiatus result in the same trends witnessed in 2018.

Google Advertising revenue rose 69% year-on-year in Q2 2021

Google Advertising revenue grew 69% year-on-year in Q2 2021, rising from $29.8bn to $50.4bn, a financial statement reveals. Alphabet’s total revenue, meanwhile, grew to $117.2bn during the period, up from $79.5bn in Q2 2020. The result follows a tougher-than-usual second quarter last year as the first wave of coronavirus impacted demand for advertising, thereby stunting the tech giant’s growth.

Sundar Pichai, Google’s CEO, commented that the company had seen a ‘rising tide’ of online activity between April and June this year as life for advertisers and consumers alike shifts to a new normal. Indeed, Google’s results show advertising spend is recovering strongly in most major markets, and consumers and businesses are still heavily reliant on its cloud services, with Google Cloud revenue rising 53% from $3bn to $4.6bn year-on-year. As a result, the company stated it will continue its long-term investment plan in AI and Google Cloud in order to ‘improve everyone’s digital experience’ in an increasingly digital society.

Alphabet also said in its statement that revenue for YouTube reached $7bn during the three months ending June 30th, a figure that continues to close in on Netflix, which posted $7.34bn in revenue in a press release on July 20th. Analysis from MarketWatch indicates that YouTube is, in fact, growing at a rapidly higher rate than the Netflix, given its broader audience, and could see quarterly revenues surpass its rival in the near future.

Digital advertising accounts for more than 40% of UK marketing budgets in 2021

Digital advertising now receives 40.7% of UK marketing budgets, up 18.5 percentage points since 2015, according to Scopen’s Agency Scope UK 2021/22 report published in partnership with WARC. A further 37.5% share of marketing budgets is put towards above-the-line actions, while 21.8% is spent on below-the-line actions.

Analysis has also found UK digital marketing budgets are higher than the average 35.7% share of budgets recorded across ten other major markets which serve as a benchmark, following a strong year and a half of digital growth in the country.

Six in every ten marketers prefer to work with specialist agencies when it comes to focusing on dedicated marketing channels like digital. The remaining four in ten say they use an integrated agency to help deliver results across a wider, more comprehensive range of marketing disciplines.

Facebook advertising revenue up 56% year-on-year in Q2 2021, but DAUs continue to stagnate

Facebook’s advertising revenue grew 56% year-on-year in the three months to June 30th, reaching $28.5bn according to its Q2 2021 results posted on July 28th. The company’s ad revenue growth is showing little sign of stalling following an increase in spend from advertisers since late 2020, once pandemic uncertainty had begun subsiding. In Q1 2021 it posted a 46% increase, while in Q4 2020 growth was recorded at 31%.

Despite this, DAUs remain stagnant, especially in Europe and the US. While overall DAUs grew by 7% this quarter, the majority of these additional 30 million users hail from the APAC region, and a smaller number from ROW, reports Social Media Today.

The data found DAUs have flatlined in the US for some time, staying at the 195 million mark since Q4 2020 and matching pre-pandemic levels in Q1 2019. US DAUs increased slightly at the height of the first peak of the Covid crisis during Q2 and Q3 2020, at 198 and 196 million respectively.

A similar story can be said for Europe, which currently accounts for 307 million DAUs, down from peaks of 308-309 million in late 2020 and the first quarter of 2021. However, Facebook has managed to retain a few million more DAUs in this region than those recorded before the pandemic hit (305 million in Q1 2020).

As Facebook’s earnings are more reliant on its core western markets, this could ‘be an important element to monitor’, says Andrew Hutchinson of Social Media Today. However, it is also worth noting that the use of other apps in the Facebook family are rising in popularity among consumers from Europe and the US, suggesting they are simply reallocating their social media time to apps like messaging service WhatsApp.

Global ad spend in Q2 2021 rose by 23.6% year-on-year, marking a new record for a second quarter period

Data from WARC has revealed global ad spend rose by 23.6% year-on-year in Q2 2021 to $157.6 billion, setting a new record high for a second quarter period and marking the strongest rate of growth in this metric for more than a decade.

Analysis shows brands are slowly recovering from the effects of the initial peak in coronavirus infections, which caused havoc on the advertising industry. Ad spend for the first six months of 2021 was 17.8% higher than the same period in 2020, totaling $311.5 billion, including a healthy 12.5% year-on-year growth throughout Q1 2021.

Throughout 2020, data has found ad spend on offline media like print, radio, TV and cinema, fell by around one-fifth – the worst performance for this sector since WARC began its analysis 40 years ago. Meanwhile, online ad spend grew by 9.4%, rising to 27.4% within the ecommerce sector and 18.3% on social media.

Consequently, WARC expects investment in advertising will bounce back at a 12.6% growth on last year, compared to the 6.7% previously forecast, while it predicts an 8.2% rise during 2022. Ad spend on ecommerce could rise as high as +35.2% year-on-year by the end of 2021, spurred on by increasing consumer demand on online retail giants like Amazon. Spend on search could see an uplift of over 26%, while online video and social media could also reap a 17.7% and 13.1% growth respectively.

GroupM revises global advertising growth prediction upwards to 19% midway through 2021

Advertising growth for the year so far has exceeded prior expectations due to the ongoing effects of the pandemic on the industry. As a result, in June, GroupM had to revise its previous predictions upwards to reflect this trend. Now the company expects global advertising growth to reach 19% by the end of 2021 (excluding US political advertising), up significantly on the 12.3% growth first predicted in December 2020.

This equates to a 15% rise in total ad revenue compared to 2019 results, with similar levels of year-on-year growth expected in the coming years as the world recovers from the pandemic. By 2026, GroupM estimates the global advertising market to hit the $1 trillion mark – a huge increase from the $641 billion reported in 2020.

Zooming in on individual markets, several regions including the UK, India, China and Brazil are anticipated to see more than 20% growth in 2021 compared to the year before, while others like the US, Canada and Australia could experience an uptick in the high teens. Meanwhile, as digital advertising becomes more prominent, there may now be a 26% growth rate for pure-play digital media in store this year (up from a predicted 15%).

One of the most notable shifts in GroupM’s projections is in audio advertising. It now envisages this sector to achieve growth of around 18% versus prior predictions of 8.7%, thanks to increased uptake in this format from consumers. However, even if audio advertising meets these lofty expectations this year, it still won’t be enough to fully recover from the 27% decline recorded last year.

Five tech companies accounted for 46% of global advertising revenue in 2020

Five major tech companies – Google, Facebook, Alibaba, Bytedance and Amazon – accounted for nearly half (46%) of global advertising revenue in 2020, equating to $296 billion. Google came out on top, taking a 21% share of total revenue during the year, followed by Facebook at 14%, while Alibaba ranked third at 4.5%. This is according to analysis from GroupM’s June 2021 report ‘This Year, Next Year Global Mid-Year Forecast’.

In contrast, the top five companies in 2019 garnered $247 billion, a nearly 38% share of global ad revenue, demonstrating just how much marketers’ advertising choices during the pandemic have shifted in favour of big tech. Notably, Comcast’s ad revenue was still more than that of Amazon’s back in 2019.

Nearly a decade prior (2010), the five largest brands for ad revenue – then Google, Viacom/CBS, News Corporation, Comcast and Disney – claimed just a 17% share of revenue. Comparing the numbers, and indeed the types of companies listed in the top five, we can see a dramatic change in the worldwide media landscape in a relatively short time. There is no doubt that the pandemic has played a substantial part in accelerating the advertising revenue growth of many of these already dominant companies in 2020.

Amazon Advertising CPC is up by more than 50% year-on-year

Analysis from Marketplace Pulse reveals Amazon Advertising costs have soared in the past year as the ecommerce giant becomes an ever more popular place for consumers to shop and retailers to sell their products to a global market.

On average, cost per click on the site reached $1.20 in June 2021, up from $0.93 at the start of the year (a 30% growth) and rising more than 50% compared to June 2020, where rates were recorded at $0.79. While Amazon’s advertising rates have increased to meet higher demand from sellers, it is thought that the delayed Prime Day, which occurred in October last year, combined with Black Friday/Cyber Monday and the holidays helped to boost CPC at the end of 2020, before it continued to rocket in the first half of 2021.

Marketplace Pulse says it has watched more and more brands invest their budgets into Amazon advertising, allowing them to compete more effectively for ad space. As a result, typical customer acquisition costs for brands selling on Amazon has risen from a 15% equivalent transaction fee per order to ones that are typically more than 20%.

The study indicates that the rise in cost per click and for customer acquisition has affected all advertising types offered by the marketplace, and has been mirrored beyond the US into its global markets.

Pent-up demand for experiences and events creates increased sponsorship opportunities for brands

Data from Momentum Worldwide shows that pent-up demand for experiences and events could pose increased opportunities for brand sponsorship deals as lockdown constraints are loosened. Forty-eight percent of consumers that took part in a May 2021 study said they were planning to try new experiences this year, while another 41% said they hoped to try even more experiences than they did before the pandemic.

Currently, 40% of UK consumers say they are ready to return to live experiences and events one month after they’ve been vaccinated against Covid-19, ranking them the second most enthusiastic group behind the US (46%). On average, 35% of the global population say the same.

Consequently, many consumers believe brands should step up sponsorship deals to ensure such events take place as planned, particularly when it comes to sports fixtures. Sixty-nine percent agreed that now, more than ever, sports need brand sponsorships, while another 72% agreed that brands should focus on sponsoring teams and leagues in order to help sporting communities.

With 74% of consumers stating they’d ‘keep an eye’ on the ways brands step up to the plate in this regard, the pressure is mounting on them to play a vital role in helping fund a return to live events

FinTech marketers invested $3 billion on user acquisition in 2020

AppsFlyer’s June 2021 report, The State of Finance App Marketing, found downloads of FinTech apps rose 129% in the UK between Q1 2020 and Q1 2021, as consumers sought alternative ways of interacting with financial services providers.

Marketing-driven installs of these apps grew by 300% in the UK over the same period, significantly further ahead than records from other areas of Europe, where average growth was measured at 170%. The reason for this trend, which is occurring in large parts of the world, is because FinTech marketers have invested a total $3 billion in running ‘aggressive’ user acquisition campaigns over the last year, the study explained.

Demand for investment apps has rocketed in the UK, with installs growing 61.4%. This could be driven by an increased spotlight on zero commission investment apps like Robinhood, which gained traction with amateur investors in late 2020. Meanwhile, globally, installs of apps from digital banking providers have increased 45% year-on-year, and installs of apps offered by traditional banks rose 22%.

Twenty-nine of the top forty financial services apps on all app stores experienced at least a 20% increase in downloads between early 2020 and early 2021, while the average number of downloads in developing countries was 70% higher than those of developed countries. These figures indicate a rising demand for FinTech apps across the world, regardless of market size, as people manage their finances on online platforms throughout the pandemic.

Data shows UK media quality has been compromised amid Covid-19

Integral Ad Science’s Media Quality Report H2 2020, published in April 2021, reveals UK media quality has been compromised amid the unprecedented circumstances of the last year.

The data, which examines advertising campaigns that ran between 1st July and 31st December, shows UK brand risk increased across all media environments analysed (mobile and desktop display and video) compared to the same period in 2019. Desktop display brand risk rose the most over this time, jumping 3.2% to 5.8%, representing the highest level of brand risk in this environment since 2017, a year laden with brand safety controversy. Meanwhile, brand risk on mobile video rose to 8%, making it the highest risk environment of all, but it experienced the smallest change at +0.2% year-on-year.

Of all factors that contributed to this worsening brand risk, hate speech saw the highest rise in share. The share of desktop videos flagged for this issue grew from 0.6% in H2 2019 to 16.5% in H2 2021, and from 2.2% to 17.1% on desktop display.

Additionally, adult content on desktop display made up 18% of all pages flagged for brand risk (up from 3.5%), while share of violent content grew from 10.4% to 21.3% year-on-year. Violent content on mobile display, however, improved significantly, shrinking brand risk in this category for this environment from 40.2% in H2 2019 to 27.3% in H2 2020.

Q1 2021:

76.2% of European consumers have consumed more audio content since the pandemic started

A comprehensive Audio Content Survey from Sortlist in April 2021 shows, on average, 76.2% of European consumers have consumed more audio content since the pandemic started than they did before. The research on listening habits was conducted on 500 business leaders of small to medium sized enterprises across France, Germany, Spain and the Netherlands.

Radio was the most preferred type of audio content among those surveyed, reaching its highest in Spain at 56.1%. This was followed by podcasts, which seem to be less popular in the Netherlands (30.1%) than they are in France (40.9%). In fact, there was just a 5.2% gap between the popularity of radio and podcasts in France. With 900,000 new podcasts created in 2020 alone (a 300% year-on-year rise), the popularity of podcasts could increase even further, and perhaps overtake radio, in certain regions in the near future.

Across the board, consumers are much more likely to listen to audio related to their hobbies than their day jobs. Other popular topics include news-related content, audiobooks and other miscellaneous entertainment.

The data also reveals some good news for advertisers using audio formats for their campaigns. Seventy-eight percent of survey respondents said they have bought, or are open to buying, products promoted alongside the audio content they listen to.

UK ad market expected to be the second highest for growth in 2021

Ad spend in the UK could grow at the second highest rate of all global markets in 2021, Dentsu’s Ad Spend Report 2021 predicts. Dentsu expects a healthy recovery for the UK ad market, forecasting a 10.4% year-on-year growth by the end of 2021, with only one other region – India – in front at +10.8%. France, Canada and Italy will also experience healthy growth at 8.9%, 7.2% and 5.9% respectively.

While the US will continue to dominate the total share of global ad spend (37.9%), the UK ranks fourth in this area with a modest 5.1% share, also behind China (17.6%) and Japan (9.9%).

Understanding and predicting which new consumer behaviours will be temporary, and which will be permanent, will be the largest challenge for advertisers in the coming year. However, brands appear to be confident that social, search and video will be the biggest drivers of digital growth in the sector, despite the global outlook remaining uncertain in the first six months.

European digital ad spend rose 6.3% in 2020

European digital ad spend rose 6.3% in 2020 to a total €69.4 billion and overall digital share of advertising grew to 56.5%, according to analysis from IAB Europe. This result was substantially lower than the average annual growth rate since 2006 (19.5%) and notably smaller than the 8.9% increase posted in 2009 – the last financial crash – demonstrating just how much the pandemic has affected the sector.

Four of the twenty-eight markets analysed saw a decline in digital ad spend over the course of 2020, however, in contrast, seven saw double-digit growth despite one of the rockiest years on record. Turkey came out on top, posting a 34.8% growth, followed by Ukraine (26.5%) and Serbia (19.2%). Meanwhile, the UK saw results below the European average for the year at 5.1%.

Drilling down, display advertising experienced a healthy increase over the period at 9.1%, with social display advertising growing 15.9% to €16.1 billion and other display increasing a more modest 2.9% to €15.6 billion. 2020 also marked the first year social has occupied a larger share of display advertising spend than all other display advertising spend combined.

Additionally, the last year saw a prominent shift towards video display advertising, up 10.1%, and a decline in investment in formats like banners and static images (down 1.1%). Audio, in the meantime, continued to occupy a very small percentage of ad spend by comparison to other categories, but grew at the fastest rate of 16.7%, mirroring recent trends.

Top ad agencies make modest predictions for growth of global ad market in 2021

At the close of 2020, Forbes compiled predictions from three top ad agencies, Magna, Zenith and GroupM, on the potential growth of the global ad market in 2021.

There appears to be a consensus that digital advertising will grow at a faster rate than traditional forms of advertising. Cinema advertising is also set to make a steady comeback this year as some regions roll out vaccinations and lift restrictions in an attempt to help life return to normal. With the Olympics in Tokyo on track to take place after being delayed last year, sports advertising will likely see a boost, too.

Magna says it expects to see global ad spend to rise 7.6% in 2021 to $612 billion total, with digital media seeing growth of 10.4% and linear media a much more modest 3.5% (although $42 billion less than in 2019). It also predicts India to be the leader of total ad spend growth across the globe, up by 26.9% year-on-year.

Zenith, meanwhile, predicts global ad spend will reach $634 billion – still less than the total recorded in 2019 – and then by another 5.2% in 2022 to $652 billion. After a big boost from the recent 2020 election, the US could see quite a small growth in ad spend this year, at just 3.3%, compared to other regions like Latin America and the Middle East/North Africa at 10-11%.

GroupM is the most optimistic about the ad market in 2021, forecasting a jump to $651 billion, with the largest rate of growth in Latin America (24.4%) and APAC (14.1%). According to their analysis, digital media could see a 14.1% total rise to $396.8 billion, significantly higher than figures estimated by Magna.

FMCG brands are re-evaluating media strategies as consumers shift to online grocery shopping

Only 23% of executives are confident in the speed at which they’re gaining accurate insights

Only 23% of executives believe the speed at which they gain accurate insights is ‘very strong’, the Digital Trends 2021 report from Econsultancy and Adobe reveals. This explains why agility has been ranked as the second most important development objective for mainstream organisations moving forward, just below innovation.

Data also suggests there is a strong link between the rating of an organisation’s insight agility and the projected budget increases over the next year. Fifty percent of companies that were reported to have a ‘strong’ speed to customer insight are planning a 2021 marketing budget increase in a continued time of uncertainty, as employees are more able to prove the value of marketing within their individual organisations.

Furthermore, 52% and 44% of ‘strong’ respondents, respectively, said they will be expanding their acquisition and retention budgets this year, compared to just 39% and 30% of those with a comparatively ‘weak’ speed to consumer insight. Meanwhile, thanks to their more in-depth analysis of customer insight, CX leaders are significantly more likely to increase their marketing budgets for 2021 (60%) than CX mainstream organisations (39%).

Q4 2020:

Disney’s D2C ad revenue grew 47% in Q4 2020

Ad revenue via Disney’s direct-to-consumer channels, which include online streaming services Hulu and ESPN+, grew 47% year-on-year in Q4 2020, to $882 million, Bloomberg reported in March. This means these revenue streams are close to catching up with, or indeed surpassing, ad revenue recorded by its major linear broadcasting networks like ABC, which saw only a 5% growth over the same period (to $984 million).

The disparity in growth reflects the huge shift in consumer preference towards streaming services versus more traditional forms of television, as accelerated in part by the coronavirus pandemic.

Hulu, which now has more than 39 million subscribers, has created new technology that allows advertisers to be able to buy ads themselves using data, collected by Disney, that indicates what audiences are watching across their owned channels and when. As a result, marketers can make more informed decisions on where their campaigns would best fit within Disney’s ecosystem.

Consequently, Disney says it expects an 80% uplift in automated ad revenue from its online channels by the end of the year. In time, this method could also be implemented across Disney’s traditional channels too: the company believes that, in five years’ time, up to half of its total ad inventory could be bought by marketers in this way.

Global ad spend predicted to have fallen 10.2% year-on-year in 2020

In a November 2020 report, WARC predicted that 2020 global ad spend will fall 10.2% to $557.3 billion compared to results from 2019. The ongoing fallout from the pandemic has meant that traditional media has had its worst year on record and this has had an enormous effect on the industry as a whole.

Drilling down by industry, ad spend in automotive is expected to decline the most severely overall in 2020, with a loss of $11 billion. Travel and tourism could see ad spend drop by a total of 33.8%, but looks set to rebound at the fastest rate next year at +19.5%. After a very volatile year, total retail ad spend could fall 16.2% to $54.3 billion and is only projected to rebound with a 5.9% growth next year – a much slower rate than some other verticals like automotive (predicted +14.1%) and media and publishing (+8.4%). Business and industrial could also struggle, as its forecast growth of 5.3% means investment in this sector could only increase by 2.5% on 2019.

Consequently, WARC says it could take up to two years for ad spend to fully recover to levels seen before the onset of the coronavirus. According to analysis, a 6.7% growth in ad spend throughout 2021 will only be able to make up for 59% of losses that occurred this year. In 2022, ad spend would need to rise a further 4.4% to finally meet 2019’s $620.6 billion.

H1 2020:

UK digital ad spend fell 5% year-on-year in H1 2020

Research from IAB UK, as reported by WARC, has found that UK digital ad spend fell by 5% in H1 2020 compared with figures from the first half of 2019.

Across the sub-categories within the digital marketing sphere, some areas performed better than others. Display advertising grew by 0.3% year-on-year to £2.84 billion, within which video advertising rose 5.7% mirroring increased engagement consumers had with video streaming services over lockdown. Without video’s strong growth, overall digital ad spend results would have been much worse.

Search ad spend, meanwhile, dropped by 3.7% during this period, representing a £143 million fall in revenue on H1 2019. Mobile ad spend also saw a decline, but a much more modest 1%. However, one of the worst affected areas of digital ad spend was classifieds, which saw a massive 33% fall in revenue, decreasing by £235 million to £485 million.

Q2 2020:

Biggest recorded drop in UK marketing budgets takes place in Q2 2020

The net balance of organisations that have cut marketing budgets fell to -50.7% in Q2, down from -6.1% in Q1. This latest figure is the biggest drop recorded by the IPA Bellwether Report since the report began twenty years ago – including the Q4 2008 financial crisis when marketing budgets were slashed to -41.7%.

Nearly 64% of those surveyed stated they had recorded a decrease in marketing spend between April and June, compared to 25% who recorded a decrease between January and March. Just 13% said they had seen an increase in budget for the same period.

Drilling down, a net balance of -76.6% of organisations reported cuts to their events marketing budgets in Q2, with just 3.6% claiming they had risen. Meanwhile, the reduction in main media budgets dropped to a net balance of -51.1%, the largest decline seen by the report for this metric. Out of all subcategories in main media marketing, OOH budgets unsurprisingly were hit the hardest (-61.2%), followed by audio (-50.0%) and published brands (-49.2%).

Direct marketing and PR budgets were least affected in the second quarter, but still recorded a severe downturn in net balance to -41.6%.

JC Decaux revenue down 63% in Q2 2020

In its H1 2020 results, JC Decaux stated its revenue plummeted by 63.4% in the second quarter of 2020, a figure it claimed was ‘historic’ for the company. OOH advertising has taken a huge hit from lockdowns and stay-at-home orders around the world and JC Decaux’s data reflects the extent of financial losses felt in the industry.

In Q2, the company reported €351.9 million in revenue, down from 1 billion during the same period in 2019. Revenue in Q1 was less badly affected, but still recorded a 13.1% year-on-year drop from €840 million to €723.6 million. Overall revenue for H1 2020 was down by 41.6%.

When it comes to revenue via geographic area, most regions saw relatively similar year-on-year declines. France and North America faired the best with -37.1% and -38.3% revenue growth respectively, while ROW and APAC saw the worst revenue declines of -48% and -43.7%.

The company said it has scrapped its earnings guidance for 2020 in light of the ongoing disruption and uncertainty caused by Covid-19.

Global mobile ad spend soared 71% in Q2

PubMatic’s Mobile Quarterly Index found that mobile ad spend soared 71% year-on-year during Q2, rising to 77% in the Americas, as spending across other areas was slashed.

While APAC experienced lesser year-on-year growth than other geographical areas (+66%) its 30% quarter-on-quarter growth was particularly strong, reflecting both the increasing cost of ads in the region and its advanced position in the timeline of the global pandemic. This could indicate that APAC will see the strongest immediate recovery in this metric as the outbreak subsides.

Despite being heavily impacted at the start of the outbreak, mobile video platform spend has seen a strong and steady recovery since the end of April and is now measuring 116% up on pre-pandemic levels in the US. As of Q2 this year, mobile now has a majority share of video ad spend across APAC (74%), EMEA (70%) and the Americas (60%).

Customer experience

30% of UK B2C companies are still not back to pre-pandemic CX levels

A September 2021 report on the state of customer experience in the UK reveals as many as 30% of B2C companies have not yet returned to pre-pandemic customer experience levels. The 2021-2022 UK Customer Experience Decision-Makers’ Guide from Enghouse Interactive and ContactBabel surveyed 211 organisations and more than 1,000 consumers for their thoughts on how the pandemic has affected customer experience, as well as what’s in store as companies prepare for the year ahead.

More than two-thirds (68%) of respondents claimed that higher-than-usual contact volumes from consumers is the most significant barrier that is preventing them from providing optimal customer experience. Ranked second was a lack of contact centre staff (62%), while a reduced operating budget (43%) was the third most cited issue.

Those organisations that fall into the retail, telecommunications, media and technology (TMT), and outsourcing sectors were the most likely to have experienced an uplift in the number of customer service calls received.

As for the reasons why, 81% of survey participants either strongly agree or agree that there is a greater need for reassurance and confidence in their organisation’s products or services, given continued uncertain circumstances. Interestingly, more than half (54%) also say that their brand’s self-service functionality is not delivering what customers need and another notable 39% also admitted that the same could be said for their digital channels.

Travel app downloads in Europe rebound to 143 million in H1 2021

A report from SensorTower has found travel apps have rebounded substantially in European markets during H1 2021, reaching 143 million downloads over the period. While this is notably higher than in the first half of 2020, it is still 47 million below downloads recorded 2 years earlier, showing consumers remained cautious of journeying abroad.

Despite this, momentum appears to be picking up so far in H2 2021, as the vaccine rollout continues and consumers gain confidence in returning to ‘life as normal’. In August, total monthly travel app downloads met pre-pandemic levels for the first time since the coronavirus crisis began.

Much of this recovery over the summer was driven by urban travel apps, as evidenced by Uber dominating the top travel download charts, as well as keen interest in rivals Bolt, Yandex Go and CityMobil. In fact, analysis reveals downloads of urban travel apps surpassed pre-pandemic levels way back in May 2021 and have continued outperforming them in the months since.

The same can be said for accommodation apps, although numbers have dipped slightly now that the peak summer season has passed. Airbnb was one such brand in this category that experienced higher app downloads in 2021 than it did in 2019. This is reflected in its recent Q2 2021 financial results, which reported a 300% year-on-year uplift in revenue, equating to a 10% increase versus pre-pandemic financials. The brand’s share of installs, however, has decreased by 11 percentage points this year to 67%, thanks to the increasing popularity of smaller competitors like HomeAway, Holidu and HomeToGo.

Some consumer markets have upped their in-app hours by as much as 45% since 2019

Q2 2021 data from App Annie reveals a huge shift in in-app activity for mobile users over the course of the last two years, largely driven by the pandemic. Consumers in eight of sixteen regional markets studied now spend more than four hours using apps everyday. Brazil totted up the most time at an average of 5.4 hours per day, followed by Indonesia at 5.3 hours and India at 4.9 hours. Meanwhile the UK ranked tenth with an average of 3.8 hours in total.

This data suggests new habits formed during prolonged periods of lockdown in 2020 have been mostly sustained through to 2021, as time spent interacting with mobile apps has notably increased across the majority of markets compared to pre-pandemic levels. Global spending on apps in Q2 2021 also rocketed to $34 billion, up $7 billion year-on-year, and $2 billion quarter-on-quarter.

Russia, while coming in at 11th for Q2 2021, saw the largest growth in time spent in-app, up 45% on its reported data collected in 2019. Meanwhile, Turkey (ranking 6th)) saw the second-highest rise at 40%. Consumers in the US, by comparison, saw a lesser 20% growth over the two-year period, largely driven by recent downloads of apps that have no relation to Covid-19 or contact tracing, a trend separate from other countries. For example, between Q1 and Q2 2021 the app that experienced the highest download growth in the US was PictureThis, with which users can photograph a plant and find out more about it. In contrast, the NHS App, TousAntiCovid and CovPass continued to place at the top of the list in their respective regions (the UK, France and Germany).

Cryptocurrency investments and AI-driven banking become new trends in US personal finance as remote banking habits take hold

Data from SYKES observes changes to US personal finance habits one year on from the start of the pandemic. Results show mobile banking is on the rise amongst consumers, although there remains a place for in-person banking moving forward.

For example, more than half (55%) of US adults claim to have visited a bank branch in the last year to carry out tasks like depositing money or opening a new account. Of those that didn’t visit a bank over that period, 58% said they stayed away because all of their banking needs could be met online.

The recent uptick in interest surrounding cryptocurrency has also made its way into consumer banking trends of late. One in four US consumers surveyed said they had moved funds from a primary savings account into a cryptocurrency wallet since the start of the pandemic. While four in ten would never replace their primary accounts with cryptocurrency investments, 27% said they were already in the process of doing this, and a further 21% said they would consider it.

As remote banking becomes easier over time, many say they would be comfortable with taking financial advice from AI entities like robots, or an automated system. More than half of consumers (50.5%) would be happy to transfer money following guidance from these sources, according to the study. Another 48.5% would also feel comfortable depositing and withdrawing funds from their accounts, although there is less confidence around carrying out more crucial tasks like applying for loans and mortgages using this method.

Consumer confidence in June 2021 at highest level since 2016

As of June 2021, consumer confidence is now at its highest level since 2016, as UK citizens become more optimistic about the future post-Covid. A YouGov poll has revealed that overall consumer confidence index gained 3.1 points on the month before, reaching 113.6 (up from a negative 96 points 12 months ago).

Outlooks on job security and personal finances for the next year have hit record highs, which could point at a healthy amount of disposable income ready to be spent with retailers, entertainment venues and the like as they look to recover their losses from the pandemic. Typically, households are optimistic that their improved financial situations will continue over the next 12 months, and the same can be said of their expectations about house prices.

Employees are also feeling positive about workplace activity. Confidence in this area grew to 127 on the index, up by 3.8 points on May 2021 – reaching the highest level recorded in the last five years. This barometer mirrors of a number of other reports which suggest demand for products and services is booming as lockdown restrictions lift further.

Overall, not a single metric decreased compared to the month before, reflecting a changing public mood and a more positive outlook for brands and businesses.

3.7 million UK adults used online banking for the first time during the pandemic

Covid-19 has been the most major factor in the widespread adoption of digital services over the course of the last 18 months. New research from SYZYGY, which monitored digital acceleration in the UK and US throughout the pandemic, has found 3.7 million UK consumers used online banking for the first time since March 2020 (to March 2021), equating to 7.1% of adults in the region. Uptake of this service was slightly less in US as a percentage of the population, where 6.7% began online banking at some point during the crisis.

Even more UK adults (13.8%) turned to online doctors for the first time, while 7.3 million began using telehealth services for new or existing health conditions. A further 7.8% started online fitness classes to stay healthy and active during lockdowns.

This rapid surge in the usage of digital services also spanned outside of essential lifestyle, financial and health categories into leisure and entertainment. Virtual visits to museums and galleries are on the rise, with 1.4 million UK consumers exploring one via a digital device since the pandemic started. Meanwhile, a massive 4.1 million began streaming movies and TV to pass the time, rising to 20.4 million in the US, and 1.8 million UK adults took up online gaming, with a further 10 million Americans doing the same.

Q1 2021:

Q2 2020:

Global mobile app downloads decrease 4.8% year-on-year in Q2 2021 as Covid-19 surge subsides

The number of global mobile app downloads totalled 35.9bn in Q2 2021, a year-on-year fall of 4.8% following the huge surge in demand during the onset of Covid-19 a year earlier, according to SensorTower’s latest Data Digest report. Apple’s App store saw an even greater 13.3% drop, while Google Play downloads fell 2.1% over the period.

Once again, TikTok was the most downloaded app worldwide, marking the fifth time it has held the top spot in the rankings in the last six quarters. In the most recent three-month period, the short-form video app surpassed 200m downloads for the first time since it was removed from India’s app stores back in the second quarter of 2020. Facebook family apps accounted for the rest of the top five downloaded apps, while video-conferencing software Zoom ranked sixth.

In the App Store, four of the five core categories analysed by SensorTower (Games, Photo & Video, Entertainment and Shopping) saw notable declines in downloads, except for Utilities apps, which grew by 4.7% year-on-year. This suggests consumers are becoming ever more accustomed to managing their household bills and energy usage via online platforms. Perhaps unsurprisingly, the Gaming category saw the largest drop in downloads this quarter, at -22.3%, largely driven by Chinese consumers as life there quickly returns to normal.

Google Play’s core categories painted a rosier picture, with increases of more than a fifth in Tools (27.6%) and Finance (25%) and smaller increases in Social (10.6%) and Entertainment (7%) – but Gaming still saw a decline of 4.4% in comparison with Q2 of 2020.

In the US, gig work apps have made a strong comeback as the vaccine rollout gains traction with the wider population. Demand for rideshare apps like Uber rocketed in Q2 2021, with downloads steadily overtaking pre-pandemic levels from Q1 2020. There were even reports of driver shortages across some rideshare companies as driver adoption returned more slowly than consumer adoption.

1.5 million more UK citizens have begun using the internet in the last year

Lloyds’ 2021 Consumer Digital Index has found 1.5 million more UK citizens have begun using the internet over the last 12 months, thanks to increased reliance on digital services since the onset of the pandemic. This equates to 95% of the UK population now being online.

Predictions cast before the onset of coronavirus suggested that it would take until 2025 for 58% of the population to obtain what is known as ‘high digital capability’, but the rapid acceleration of online activity has meant 60% now have this degree of capability in 2021.

The report found, in the last year, 72% of consumers made an online purchase from a brand they had never purchased from before, 67% visited a news website for the first time and a further 65% made their first ever video call.

Although there has been a huge uplift in digital activity since the pandemic began, a considerable proportion of UK internet users (29% or 14.9 million people) have very low digital engagement scores. This means 14% or less of their spend is online, rarely via mobile devices, and they often don’t use email or online banking services. This segment has shrunk by just 4 percentage points since 2020, and 2.6 million consumers still remain completely offline, signifying that there are still several unsolved barriers to increased digital engagement.

Data shows that those in these two groups are more likely to be older (just one in ten people who are offline are under 50 years old) and earn less than £20,000 a year. Analysis also indicates that digital poverty has been intensified by existing social and financial vulnerabilities more than ever in the past 12 months. As a hybrid online/offline approach to work and lifestyle is expected to continue past the pandemic, digital poverty and inclusivity become ever more important topics to address.

US and UK social media users most likely to advocate for a brand on price and/or value for money

A Brandwatch report on Customer Loyalty has found US and UK social media users were most likely to publicly advocate for a brand on price and/or value for money than any other purchase driver over the course of 2020. Approximately 40% of consumer brand advocacy discussion on social media platforms in these regions mentioned fair prices or good value for money over this period.

Two additional reasons were consistently cited as causes for brand advocacy by respondents – quality of products received, as well as a great delivery experience, perhaps due to the increased demand on delivery services in 2020 as customers shopped online. Each of these reasons accounted for 20% of positive brand mentions on social media.

When it comes to detraction from a brand on social media, however, consumers are far more likely to post about a poor delivery experience than anything else, followed by the negative treatment of employees and the quality of a product they received. Poor customer service came surprisingly quite far down the list but ranked above complaints about value for money.

Notably, data shows brand detraction brand post volume in the UK and US was 20% higher than the number of posts advocating brands, indicating that social media users prefer to post about negative experiences than positive experiences.

Consumers have become more trusting of brands for health and wellness advice

Consumers are becoming increasingly more trusting of brands than ever for health and wellness advice, according to data from a recent Forrester report titled The Trust Imperative.

The research indicates that consumers across the regions of the US, UK, France and India are now more trusting in brands than they are in their local and national governments and the mainstream media in their areas. In fact, close to half of consumers in the US and UK say they have faith in brands to give them advice on how to stay healthy, while an additional third (32% and 33% respectively) accept guidance from them on topics of mental wellness, like anxiety and stress.

On the other hand, if a brand goes against a customer’s strongly-held values, a growing proportion of them will stop purchasing their products or services. Just over one-quarter (26%) of French shoppers agreed they would do this, followed by 23% of those based in Singapore and 18% of those in the US.

6 in 10 UK brands don’t rank customer satisfaction as a top priority for 2021

Research from customer engagement platform Braze has found that 6 in 10 UK brands don’t rank customer satisfaction as a top priority in their 2021 business strategies.

The vaccination programme currently being rolled out offers hope that both life and business will return to normal in the second half of this year, and marketing budgets are set to rise alongside this for 50% of companies that took part in the study. However, it appears that marketers plan to prioritise this investment in Artificial Intelligence tools (47%) more than in customer analytics (45%) or customer satisfaction (43%).

With the massive disruption to customer loyalty that has been experienced by businesses across the globe in the last 12 months, this smaller than expected focus on customer satisfaction could spell trouble for brands looking to improve rates of repeat purchases and/or ROI. Although Artificial Intelligence can have some impact on the way marketers can respond to customer behaviour, which will in turn help revenue in the short term, it is equally or more important that they ensure their customers are happy with their experience to achieve long term success.

Additional data from the study highlights a further lack of precedence for customer experience among these organisations. Just 3 in 10 companies share a company-wide understanding of how to define customer engagement, while a further 77% struggle to demonstrate levels of customer engagement through tangible business outcomes. Despite this, 79% still feel confident in their customer engagement strategies for 2021.

James Manderson, GM and VP of Success at Braze EMEA explains, “While it is positive to see that UK companies are upping their marketing budgets this year, it is imperative they place it into customer engagement strategies and tools that impact revenue.

…2020 was a wake-up call to marketers who learnt that products or services alone are not enough to win customer loyalty. Today, customers are in the driving seat and want to be communicated with in a way that suits them – it’s important companies respect that and take action.”

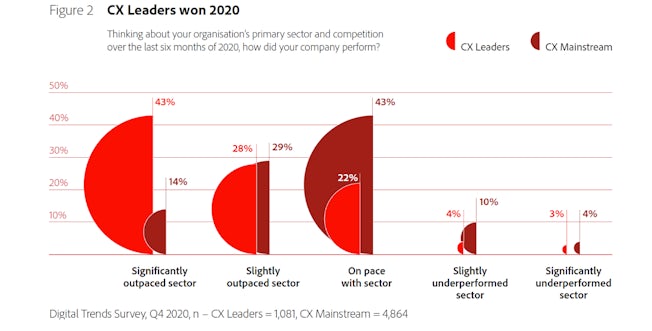

CX leaders were three times more likely to outpace the mainstream on company performance in 2020

Organisations defined as ‘CX leaders’ were three times more likely to outpace organisations in the ‘mainstream’ on company performance in 2020, according to the Digital Trends 2021 report from Econsultancy and Adobe.

In total, 71% of CX leaders (who comprised 18% of respondents and were defined as having very advanced approach to CX) claimed they had ‘significantly’ or ‘slightly’ outpaced average performance in their sector last year compared with just 43% of the mainstream (those whose CX capability ranged from ‘immature’ to ‘somewhat advanced’). Meanwhile, double the number of organisations reported to be on pace for performance were CX leaders (43% vs 22% in mainstream).

CX leaders also appear to have greater insight into the motivations and challenges that their customers are facing, due to the long-term development of their analytics functions in the years before the pandemic began. As a result, they are more than twice as likely to report that their customers have had a positive digital experience with their brand than others with lesser insight. They are also able to make more empathetic decisions, data suggests.

Fifty-three percent of CX leaders say they have detailed insight into the drivers of loyalty/retention for customers organisation, compared to just over one-fifth of companies in the CX mainstream, while similar numbers were reported across insights into mindset of customers and friction points in the customer journey.

The CX mainstream performed marginally better against its competitors when it came to knowledge of purchase drivers (25% vs. 49% of CX leaders). However, there is still plenty of room for improvement, as 60% of client-side respondents across all companies admitted that they would still ‘definitely’ or ‘possibly’ get frustrated were they a customer of their own organisation’s experience.

25% of brands will see ‘statistically significant advances’ to their CX quality in 2021

As customer experience, particularly through online channels, was thrown into the spotlight for most of 2020, renewed focus on this core business aspect will enable vast developments throughout the course of 2021, according to predictions from Forrester.

Twenty-five percent of brands will see ‘statistically significant’ advances to their CX quality next year, despite budget cuts, thanks to increasingly improving customer experience competencies on the back of short-term fixes generated at the peak of the coronavirus outbreak. As a result, this move could save companies hundreds of thousands, or even millions, of dollars, the data forecasts.

Forrester also expects spending on customer loyalty and retention will increase by 30% over the next year, after acquiring plenty of new online customers during the 2020 ecommerce boom. Brands can expect to see their CMOs taking more control over the full customer lifecycle in order to improve CLV amid the uncertain financial climate ahead. Many CMOs are likely to integrate marketing with CX to create a more joined up experiences that encourage customers to stick around.

82% of UK consumers are still recommending brands during the pandemic

Research from MentionMe reveals that, although there has been a rising trend of consumers abandoning brand loyalty over the course of the coronavirus crisis, brand advocacy remains as strong as ever in the UK.

Eighty-two percent of consumers that took part in the study said that they had recommended a brand over the last year, and more than a third have in the past month alone. Many of these referrals were for home improvement brands selling furnishings, DIY and garden products, which have also seen a huge rise in sales across lockdowns. Other sectors with high referral rates included food and drink (up 10% on 2019), subscriptions and technology, and, unpredictably, holidays and travel.

After a year of uncertainty, 65% of consumers now place the trustworthiness of a brand as the top reason for referring them to a friend or relative, followed by great customer service (58%) and free delivery or returns (51%). However, there were aspects that became much less important over this period. Brands that ‘surprise or delight’ consumers and those with innovative products, fell by 22% and 17% respectively from previous figures in 2019.

Consumers also appear to be considering the wider impact of their purchasing decisions, particularly as home delivery has become so commonplace. As a result, nearly one-third of respondents said they would be more likely to recommend companies with ‘green credentials’.

Q4 2020:

47% of British consumers have had issues with parcel delivery since the onset of coronavirus

An October 2020 survey of more than 2000 British consumers, commissioned by Citizens Advice, has found that nearly half (47%) of British consumers have had issues with the delivery of parcels since the first lockdown began in March.

With the UK having been in full or partial lockdown for much of this year, 51% say they feel more reliant on having products delivered to their homes. The increased numbers of people now shopping online, whether for necessity or convenience, seems to have thrown retailers’ logistical issues into the spotlight.